For generations, farm insurance in Australia followed a fairly predictable pattern. You arranged cover for fire, perhaps added hail if the crop justified it, renewed the policy each year and got on with the business of farming. For a long time, that approach worked well enough because weather patterns were relatively stable and the risks were easier to anticipate.

Not anymore. The problem in 2026 is that farming conditions no longer behave in predictable cycles. Across large parts of Australia, the climate has become far less forgiving, and insurance arrangements that once provided reasonable protection are beginning to look incomplete.

Recent seasonal data illustrate the challenge clearly. Large areas of south-eastern Australia and Western Australia have entered planting windows with soil moisture levels sitting near record lows, a situation that increases the likelihood of crop stress even before heat, frost, or wind damage are factored into the equation. When rainfall patterns fail early in the season, the financial risk carried by farmers increases sharply because input costs such as seed, fertiliser, fuel, and labour have already been committed long before yields are certain.

Climate Risk Is Changing the Insurance Conversation

Australian agriculture has always involved risk, but the nature of that risk has piqued noticeably in recent years. While hailstorms and bushfires still occur, growers now face a broader mix of threats, including prolonged heat events, late frosts during sensitive growth stages, extended dry periods and even unpredictable rainfall patterns.

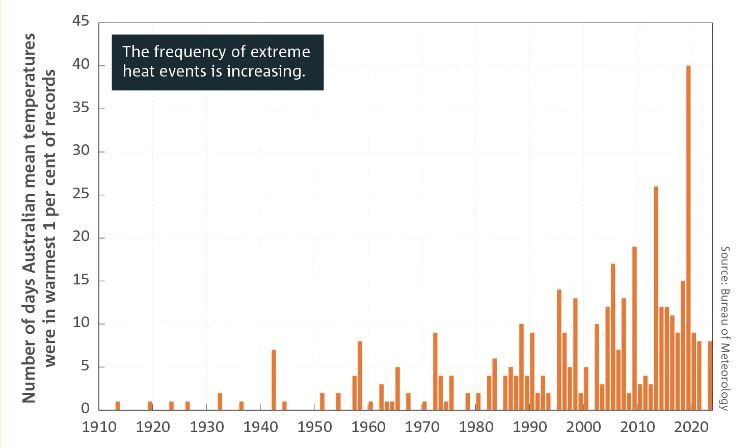

Source: BoM

The Bureau of Meteorology has reported an increasing frequency of extreme temperature days across several agricultural regions, and agronomists regularly warn that these temperature spikes can reduce yields dramatically if they coincide with flowering or grain filling periods. A single frost event during the wrong week can cause damage that fire or hail policies were never designed to cover.

At the same time, many farmers have expanded their operations or adopted higher-value crop rotations, which means the financial stakes of a bad season have grown substantially. With fertiliser shortages spiking and machinery costs climbing, the difference between a good harvest and a failed one can now mean the difference between a profitable year and a serious financial setback. In this catch-22 situation, insurance is now something that requires far more careful planning.

Why the “Set and Forget” Approach No Longer Works

One of the biggest risks farmers face is assuming their insurance arrangements still match the realities of the farm. Policies that were appropriate five or ten years ago may no longer cover the types of weather events that are becoming more common today.

Another complication is the surging premium. In 2026, several large insurers have either increased farm insurance premiums largely due to climate volatility, rising claim costs and regional concentration of risk, which have made some traditional insurers more cautious about providing broad agricultural cover as well. This is where specialist advice becomes valuable.

How Brokers Help Farmers Navigate a Changing Market

Working with experienced crop insurance brokers gives farmers access to a broader range of insurance options than they might find on their own. Rather than relying on a single insurer’s standard policy, brokers can compare multiple providers and tailor coverage to the specific risks associated with a particular crop, location, and growing season.

A good broker spends time understanding the farm operation itself, including crop types, planting schedules, historical weather patterns and the financial exposure involved in a failed harvest. With that information, they can identify policies designed to address risks that traditional insurance may overlook. For example, some specialised policies now offer protection against frost damage, extreme heat events or rainfall deficits, risks that are becoming increasingly relevant across many parts of Australia.

These policies often sit alongside more familiar cover, such as hail protection, creating a layered approach that reflects modern farming conditions rather than relying on outdated assumptions.

Another benefit of working with brokers is market access. When insurers become more selective about the agricultural risks they accept, brokers often have established relationships with niche providers who continue to offer specialised cover.

A More Strategic Approach to Farm Protection

Australian farmers have always been resilient, adapting to droughts, floods, market fluctuations and the countless variables that influence agricultural production. What is changing in 2026 is the scale and unpredictability of climate-related risks.

With soil moisture levels already under pressure in parts of the country and weather patterns becoming harder to predict, the traditional habit of renewing the same insurance policy each year without review is becoming harder to justify.

Taking a more strategic approach to farm insurance, particularly with the guidance of specialist brokers who understand agricultural risk, allows farmers to align their protection with the realities of modern farming. And in a season where the margin between a successful harvest and a difficult year can be measured in a few degrees of temperature or a few millimetres of rain, that extra layer of planning can make all the difference.